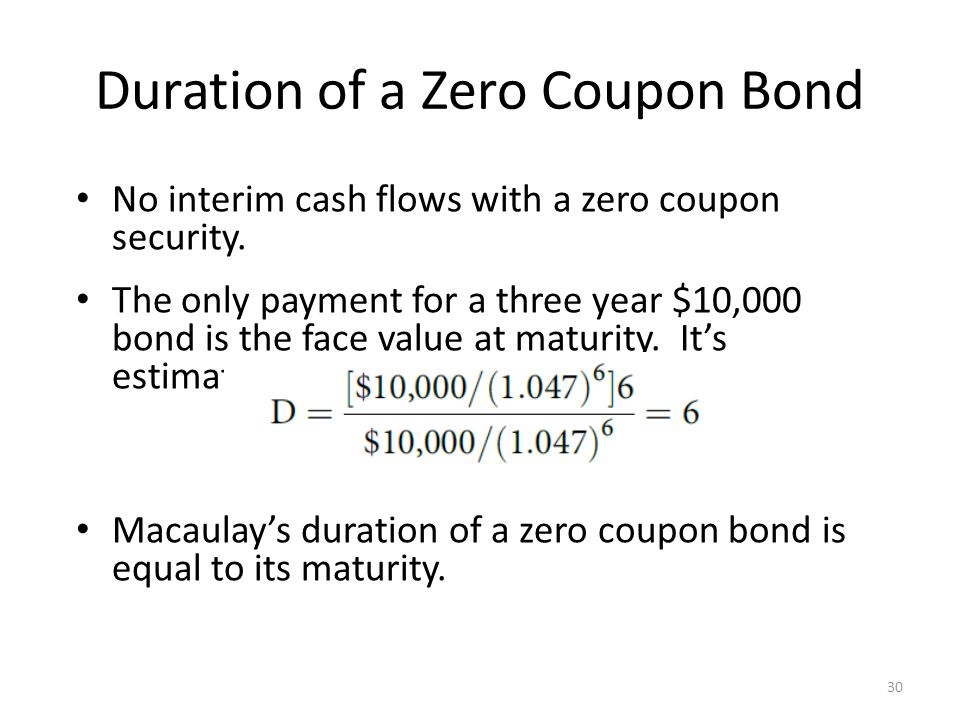

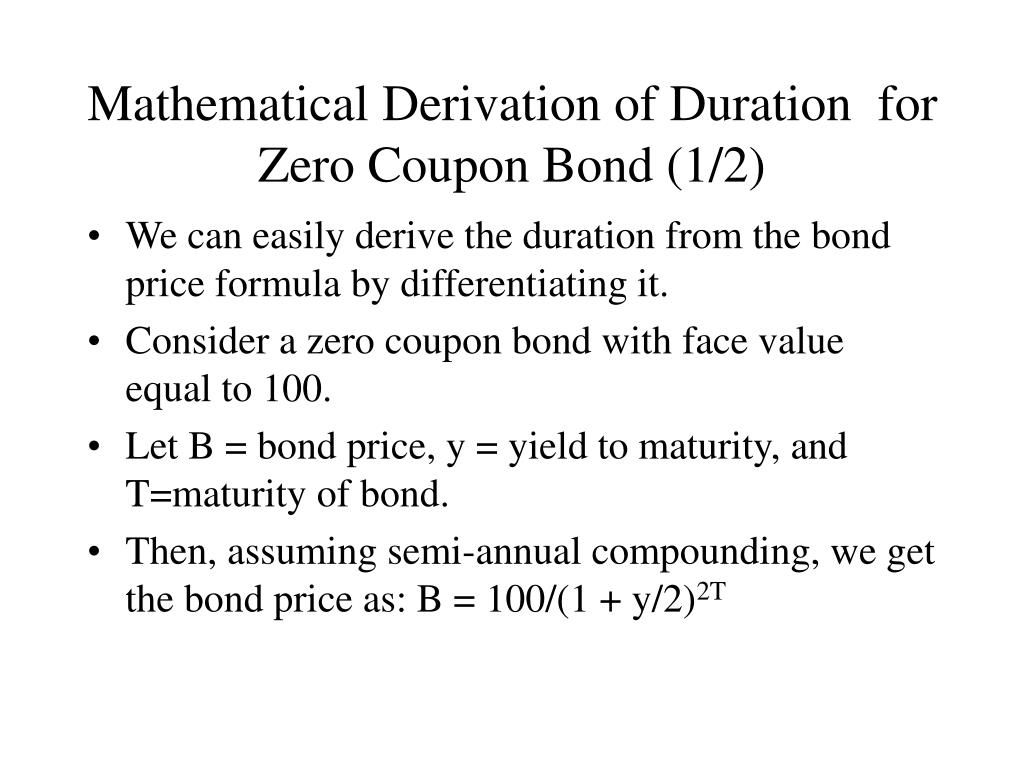

41 duration for zero coupon bond

fixed income - Duration of callable zero coupon bond - Quantitative ... fixed income - Duration of callable zero coupon bond - Quantitative Finance Stack Exchange. 1. Can anybody please help me out with the below question with a brief explanation:-. A 10-year zero coupon bond is callable annually at par (its face value) starting at the beginning of year 6. Assume a flat yield curve of 10%. Bond Duration Calculator - Macaulay and Modified Duration - DQYDJ From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity - it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5%; Years to Maturity: 3

What Is a Zero-Coupon Bond? Definition, Characteristics & Example Typically, the following formula is used to calculate the sale price of a zero-coupon bond based on its face value and maturity date. Zero-Coupon Bond Price Formula Sale Price = FV / (1 + IR) N...

Duration for zero coupon bond

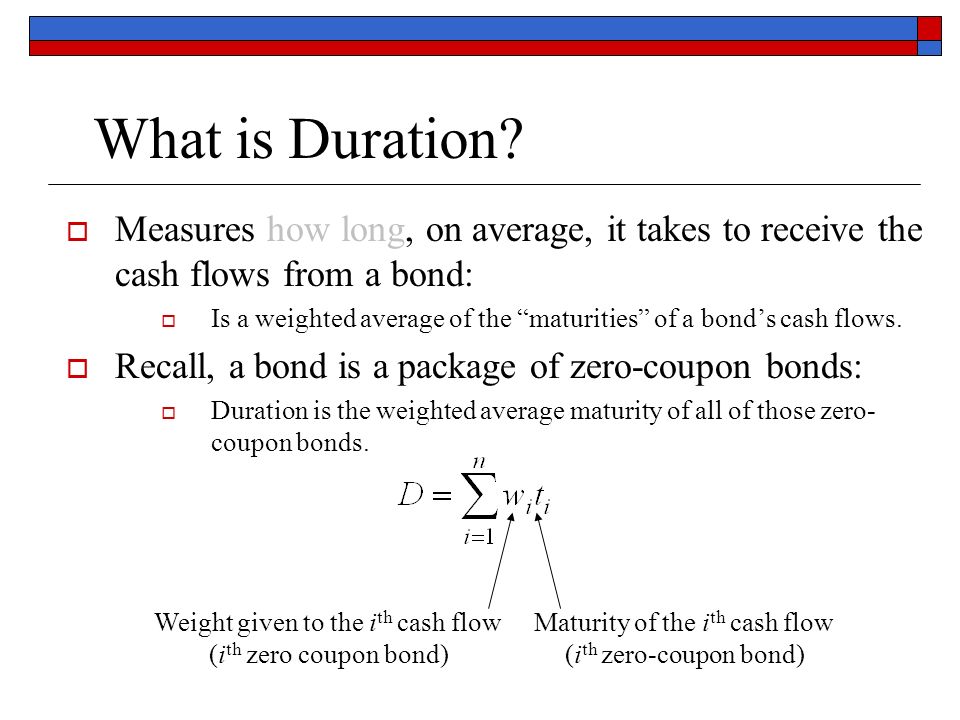

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield. Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest that will be earned over the 10-year life of ... Default Risk and the Duration of Zero Coupon Bonds This paper applies a contingent claims approach to examine the duration of a zero coupon bond subject to default risk. One replicating portfolio for a default-prone zero coupon bond contains a long position in the default-free asset plus a short position in a put option on the underlying assets. The duration of the bond is shown to be a ...

Duration for zero coupon bond. How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping n = 10 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 10%) 10 Zero coupon bond price = 508.35 (rounded to 508) In this example the bondholder has to wait 10 years before they receive the face value of the bond. Duration Of A Zero Coupon Bond - bizimkonak.com Zero Coupon Bond Modified Duration Formula - Bionic … CODES (7 days ago) We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) … Visit URL. Category: coupon codes Show All Coupons duration of zero coupon bonds | Forum | Bionic Turtle With respect to a zero coupon bond, Macaulay duration = maturity, and therefore must be a monotonically increasing function of maturity. On the other hand, DV01 of a zero (or deeply discounted) is not strictly increasing as DV01 = P*D/10,000 and the numerator has offsetting effects. If you'd kindly reference, I can fix? Thanks! Apr 7, 2012 #3 S What is the duration of a zero coupon bond? - Quora the modified duration of a zero-coupon bond is the time til maturity. for example, the modified duration of a 10-year, zero-coupon bond is ten years. if you purchase the above bond when it is halfway to maturity, the modified duration is half that, or equal to five years. Quora User.

What is the period of a zero coupon bond? | Personal Accounting The bond issuer pays interest to the bondholders for the duration of the bond's time period. Bonds are loan agreements involving creditors and borrowers. When Convertible Bonds Become Stock. ... Zero coupon bonds have a period equal to the bond's time to maturity, which makes them sensitive to any modifications within the rates of interest. ... What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... With zero-coupon bonds, the bondholders need to pay taxes associated with interest income, even though the particular gain has been realized or not. For example, with a bond that matures in 5 years, the lump sum return will only be generated at the end of the period. However, the bondholder must pay taxes, regardless of the time to maturity. Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ So a 10 year zero coupon bond paying 10% interest with a $1000 face value would cost you $385.54 today. In the opposite direction, you can compute the yield to maturity of a zero coupon bond with a regular YTM calculator. The One-Minute Guide to Zero Coupon Bonds | FINRA.org will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000.

PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of Zero-Coupon Bond: Formula and Calculator - Wall Street Prep If the zero-coupon bond compounds semi-annually, the number of years until maturity must be multiplied by two to arrive at the total number of compounding periods (t). Zero-Coupon Bond Value Formula. Price of Bond (PV) = FV / (1 + r) ^ t; Where: PV = Present Value; FV = Future Value; r = Yield-to-Maturity (YTM) t = Number of Compounding Periods Zero Coupon Bond Modified Duration Formula - Bionic Turtle Zero-coupon bonds are popular (in exams) due to their computational convenience. We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/(1+0.04/2) under semi-annually compounded yield of 4.0%. Zero-Coupon Bonds - Accounting Hub The formula to calculate the market value of the zero-coupon bond is: Price = M / (1+r) n Where M = face value or maturity value of the bond R = required rate of interest N = number of years Suppose a bond issuer needs to issue a zero-coupon bond with a face value of $10,000 with 10 years of maturity. The investors' expected rate of return is 5%.

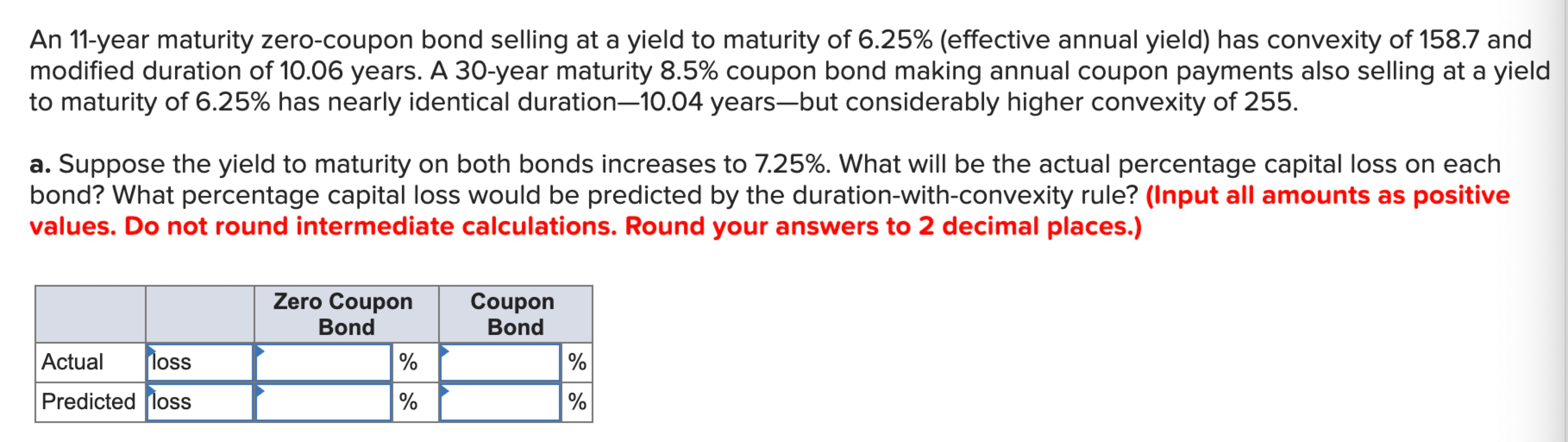

Solved An 11-year maturity zero-coupon bond selling at a ...

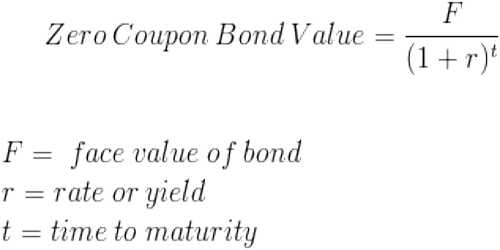

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

Chapter 11 - Duration, Convexity and Immunization

Zero Coupon Bond Calculator - Nerd Counter The formula is mentioned below: Zero-Coupon Bond Yield = F 1/n. PV - 1. Here; F represents the Face or Par Value. PV represents the Present Value. n represents the number of periods. I feel it necessary to mention an example here that will make it easy to understand how to calculate the yield of a zero-coupon bond.

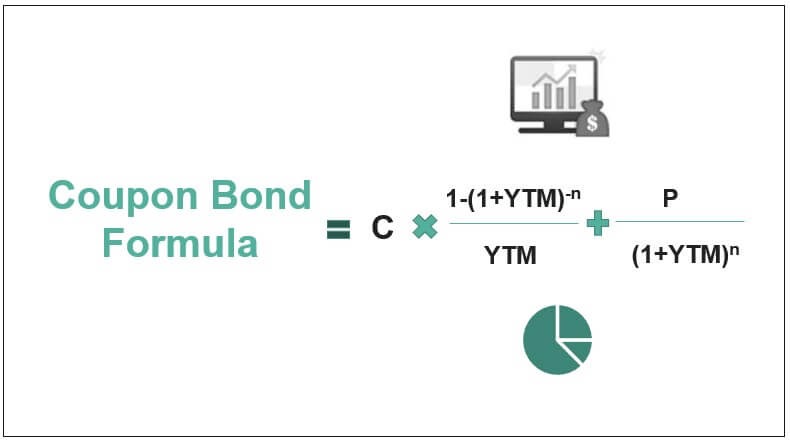

Coupon Bond Formula | How to Calculate the Price of Coupon Bond?

Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

Chapter 4 Bond Price Volatility Chapter Pages 58-85, ppt download

Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. Unlike regular bonds, ... A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms ...

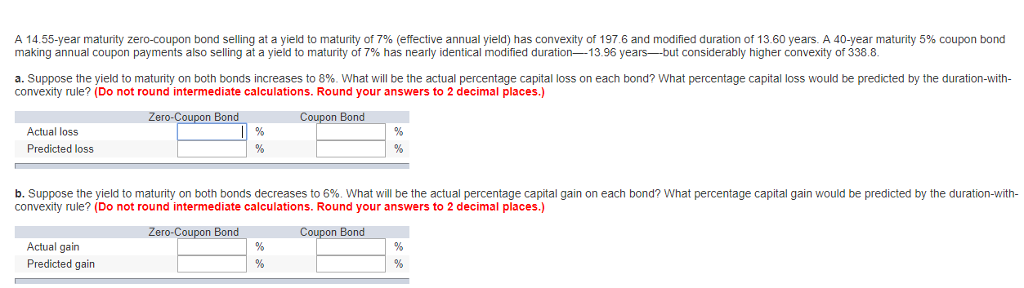

Solved A 14.55-year maturity zero-coupon bond selling at a ...

The Macaulay Duration of a Zero-Coupon Bond in Excel - Investopedia Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and...

The Key To Duration: Sensitivity To Changing Interest Rates ...

Duration and Zero Coupon Bonds - YouTube Examples of Macaulay duration are given for zero coupon bonds. About Press Copyright Contact us Creators Advertise Developers Terms Privacy Policy & Safety How YouTube works Test new features ...

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

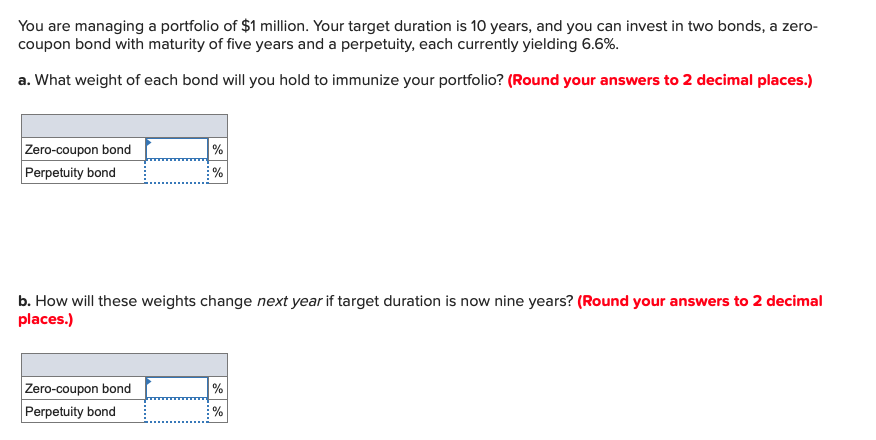

Solved You are managing a portfolio of $1 million. Your ...

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months.

Chapter 6: Pricing Fixed-Income Securities 1. Future Value ...

Duration of a callable zero bond | Forum | Bionic Turtle Consider a $100 face value 10-year zero-coupon bond that is callable (European-style) in one year at 80 percent of its face value. Figure 2.2 plots the bond's price, duration, and dollar duration as a function of yield. The bond price as a function of yield first steepens, and then flattens as yield increases (see Figure 2.2

PPT - Measurement of Interest Rate Risk PowerPoint ...

Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia Zero-coupon bonds may not reach maturity for decades, so it is essential to buy bonds from creditworthy entities. Some of them are issued with provisions that permit them to be paid out ( called)...

Bond Valuation Fuqua School of Business Duke University

Default Risk and the Duration of Zero Coupon Bonds This paper applies a contingent claims approach to examine the duration of a zero coupon bond subject to default risk. One replicating portfolio for a default-prone zero coupon bond contains a long position in the default-free asset plus a short position in a put option on the underlying assets. The duration of the bond is shown to be a ...

Bootstrapping bonds to derive the zero curve ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19. Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest that will be earned over the 10-year life of ...

Zero-Coupon Bond Definition & Meaning in Stock Market with ...

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

What is the duration of a zero-coupon bond that has eight ...

WWWFinance - Bond Valuation: Campbell R. Harvey

What Is Duration of a Bond? - TheStreet Definition - TheStreet

Solved] A 12.75-year maturity zero-coupon bond selling at a ...

Understanding Fixed-Income Risk and Return | IFT World

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Zero-coupon bond - PrepNuggets

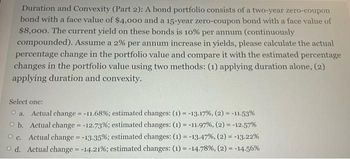

Answered: Duration and Convexity (Part 2): A bond… | bartleby

Zero Coupon Bond Vs Regular Coupon Bond - Fintelligents

Yields & Prices: Continued - ppt video online download

:max_bytes(150000):strip_icc()/DurationandConvexitytoMeasureBondRisk2-0429456c85984ad3b220cd23a760cda5.png)

Duration and Convexity to Measure Bond Risk

Duration and Convexity in Bond market

Zero Coupon Bond Value - Formula (with Calculator)

Convexity of a Bond | Formula | Duration | Calculation

Bank Management 6 th edition Management Timothy W

SOLVED:Unvolve zero-coupon bonds. A zero-coupon bond is a ...

Solved You are managing a portfolio of $1 million. Your ...

Bond duration - Wikipedia

Solved] 1) Assume you have a portfolio comprising 5 zero ...

Zero Coupon Bond Valuation using Excel

Solved A 13.35-year maturity zero-coupon bond selling at a ...

Zero Coupon Bond - QS Study

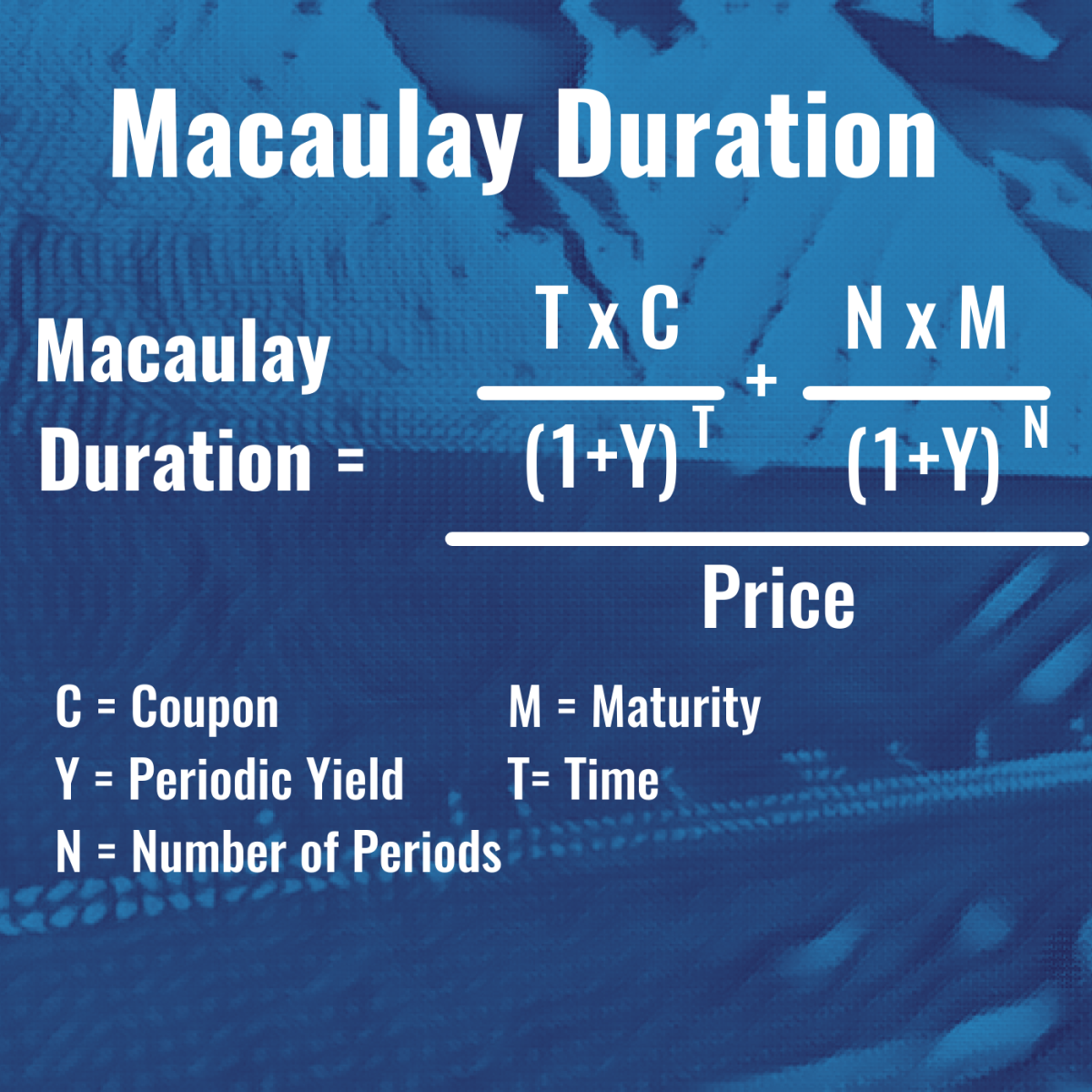

Macaulay Duration

Duration and Convexity, with Illustrations and Formulas

Duration and convexity for Fixed-Income Securities - ppt download

Bond Price Volatility Zvi Wiener Based on Chapter 4 in ...

Reserve Bank of India - Database

Post a Comment for "41 duration for zero coupon bond"